Backtesting interface

Open page: https://live.gunbot.com/backtesting/

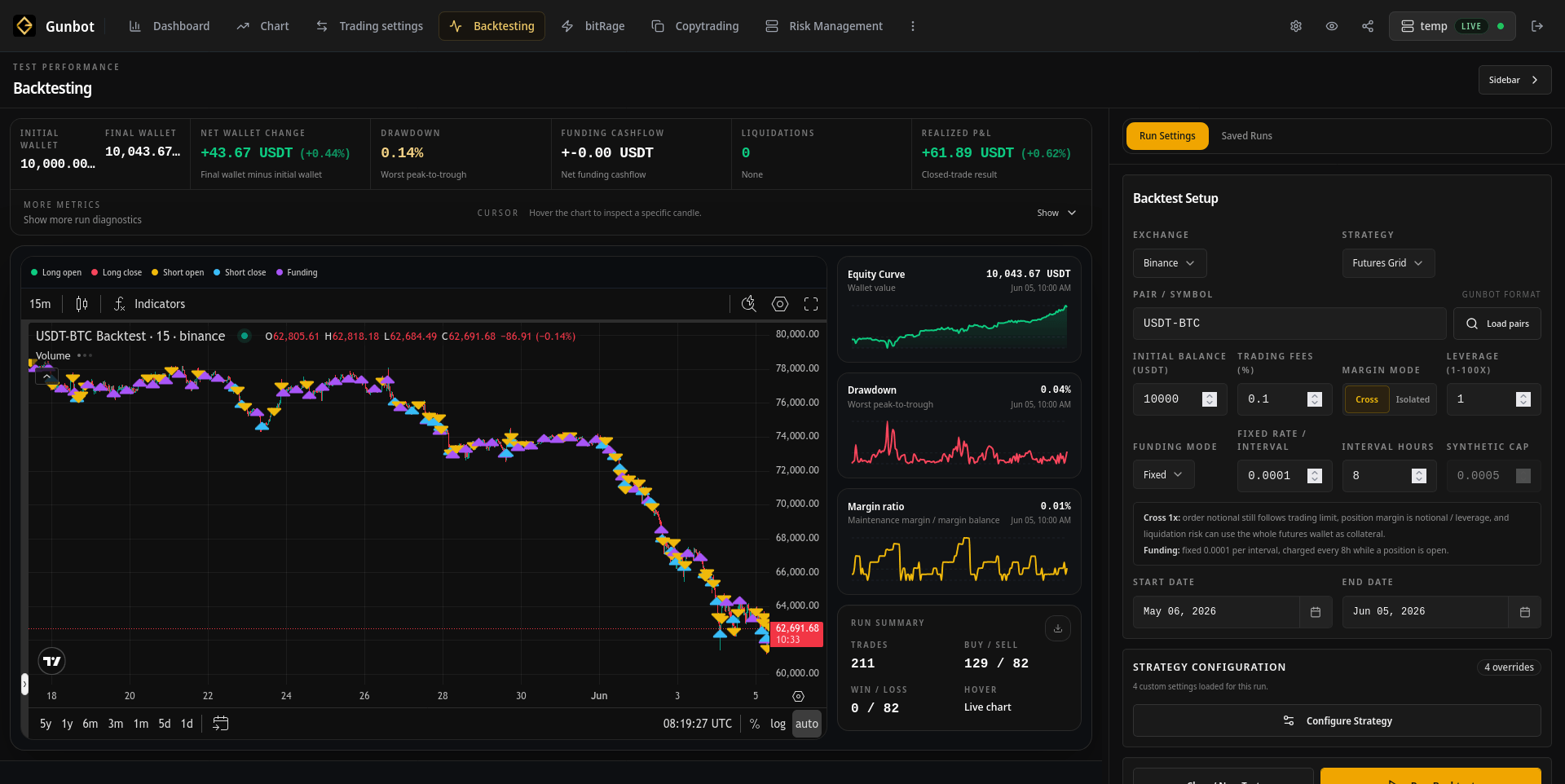

Backtesting lets you test a strategy idea before applying it to live pairs. You choose a data source, market, date range, strategy, and strategy settings, then review the resulting trades and equity curve.

What you can do here

Use Backtesting to:

- Test a strategy with historical candles.

- Change strategy settings and compare the result.

- Review trades on a chart instead of only reading totals.

- Inspect drawdown, fees, exposure, win rate, profit factor, and wallet movement.

- Save useful runs so you can compare them later.

- Turn a useful test setup into a strategy preset.

A backtest is not a promise about live trading. It is a way to reject weak settings faster and understand how a strategy behaved on known market data.

Data source and market choice

Backtesting depends on public historical candle data. That means the number of exchanges available for meaningful tests is smaller than the total number of exchanges supported by Gunbot.

If your live exchange is not available or has limited public candles, testing the same pair on a different exchange can still be useful. For example, testing USDT-BTC on a highly liquid provider can help you understand strategy behavior before adapting the idea to the live exchange.

Strategy selection and configuration

The strategy selector is the core of the page. Pick a spot or futures strategy, then open the strategy configuration area to adjust the settings that define how the strategy should trade.

Start with a small number of changes. If you change ten settings at once, the result may improve or fail without telling you which setting mattered. Test one idea, run it, review it, then change the next variable.

Visual and statistical review

Use the chart to see where entries and exits happened. Then use the metrics to check whether the result was worth the risk. A high ROI with deep drawdown may be harder to run than a lower ROI with steadier behavior.

The trade ledger is useful when the totals look good but the behavior feels wrong. Look for long periods underwater, high fee impact, too many small trades, or trades that only worked during one market condition.

Saved runs

Saved runs turn backtesting into an iteration workflow. Name useful runs clearly, compare them later, and keep the settings that actually produced the result.

How Backtesting fits the workflow

Use Backtesting before assigning a strategy to more pairs, after Dashboard shows weak performance, or before editing a custom strategy file. It is the safest place to learn from mistakes because the cost is time, not live capital.